The state of the housing market nationwide can be best described as nothing short of robust. Demand remains intense, and supply remains, well, in short supply. According to the National Association of Homebuilders (NAHB), homebuilder sentiment hit 83 in May, remaining elevated at above-average levels. Each of the past nine months has shown readings above 80, after hitting a record high of 90 back in November. Traffic also remains robust, with the Traffic sub-index hitting 73, also remaining elevated, with eight of the past nine months posting readings above 70. Readings above 50 signal builders view conditions as favorable. Average monthly inventory stands at 2.4 months’ worth of supply according to the National Association of Realtors, not far off of the record low of 1.9 months hit in December, down from 4.2 months in March 2020. These dynamics have led to higher prices, with existing home sales rising +19.1% year over year in April, with an average selling price of $341,600. Homes are selling at a break-neck pace, with the typical home sold last month spending barely 17 days on the market.

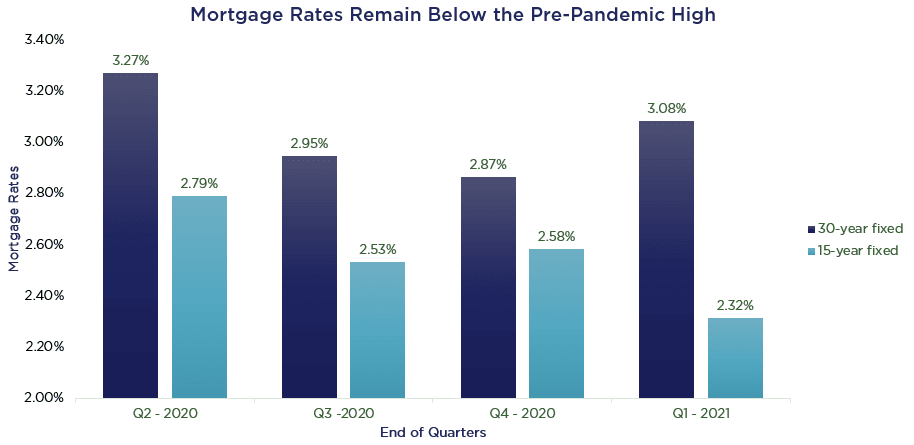

Stimulus checks and pent-up savings continue to bode well for the entire housing-related supply chain as homeowners continue to reinvest in their homes, both with added savings and stimulus, as well as for prospects of higher home values. Positive dynamics stem from more than just supply and demand imbalances. Low-interest rates should continue to persist for some time, even if they creep up slightly. According to Freddie Mac, the latest 30-year fixed-rate mortgage rate of 3.0% remained below the pre-pandemic high of 3.72% on January 2, 2020. Even if rates were to rise 0.75%, they would be just getting back to their pre-COVID highs.

Source: Nerdwallet, https://www.nerdwallet.com/blog/mortgages/current-interest-rates/; Data shown from 06/2020 to 03/2021

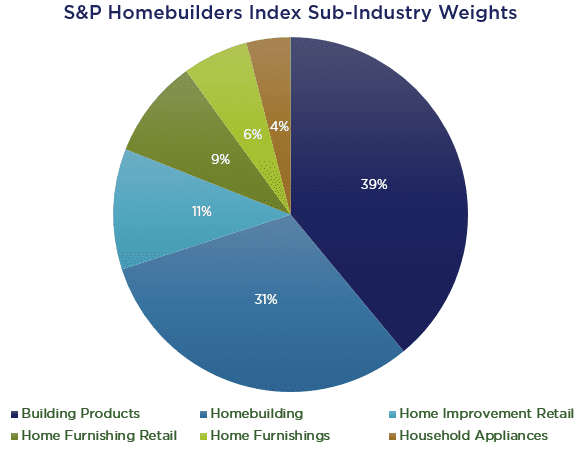

A broad measure of housing, the S&P Homebuilders Select Industry Index has been a strong performer year to date, handily outpacing the S&P 500. As of May 19. 2021, the S&P Homebuilders Select Industry Index ETF had returned +26.22% versus +10.25% for the S&P 500 ETF. Strength in the Homebuilder Index has been broad-based, coming from all sub-industry groups.

Source: SSGA, Nottingham Advisors, May 19, 2021

With quarterly earnings season nearing a close, we’ve effectively heard from the entire supply chain within the Homebuilding ecosystem. Demand remains robust for inputs (i.e. home furnishings, appliances, materials, etc.) and outputs (i.e. new homes). Inflationary pressures are generally being passed along to consumers, through higher prices and smaller square footage of new homes. Many companies are expecting margin expansion this year due to strong demand, lesser COVID related costs, and operating leverage. As such, we’ve seen a significant amount of index constituents increase their revenue and earnings per share (EPS) guidance for 2021, which continues to bode well for the entire homebuilding related category. Couple this with relatively attractive valuations and strong secular tailwinds, and homebuilding remains a favorable tactical exposure in client portfolios, not to mention a potential inflation hedge moving forward.

Matthew Krajna, CFA

Co-Chief Investment Officer

Matthew joined Nottingham in 2012 and is a member of the Investment Policy Committee. He brings over 13 years of investment experience to the team. Matthew is responsible for conducting investment research, due diligence, and contributing to Nottingham Advisors overall investment strategy. Additionally, He is responsible for establishing the firm’s strategic and tactical asset allocations. Matthew works with investment advisors and both individual clients & institutions to help build customized investment solutions to fit their needs.

Nottingham Advisors offers both institutional and individual clients experience, sophistication, and professionalism when helping them achieve their goals. With over 40 years of serving Western New York and clients in more than 30 states, Nottingham tailors each solution to fit the specific needs of each client.

For more information about Nottingham’s offerings, visit www.nottinghamadvisors.com or call 716-633-3800.

Source: Nottingham Advisors, Bloomberg, SSGA. S&P 500 ETF (ticker: SPY) and Homebuilders Select Industry ETF (ticker: XHB).

This article has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction.

Nottingham Advisors, Inc. (“Nottingham”) is an SEC-registered investment adviser with its principal place of business in the State of New York. Registration does not imply a certain level of skill or training. For information pertaining to the registration status of Nottingham, as well as its fees and services, please refer to our disclosure statement as asset forth on Form ADV, available upon request or via the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). The information contained herein should not be construed as personalized investment advice or a solicitation to buy or sell any security. Investing in the stock market involves the risk of loss, including loss of principal invested, and may not be suitable for all investors.

Past performance is no guarantee of future results. This material contains certain forward-looking statements which indicate future possibilities. Actual results may differ materially from the expectations portrayed in such forward-looking statements. As such, there is no guarantee that any views and opinions expressed in this material will come to pass. Additionally, this material contains information derived from third-party sources. Although we believe these sources to be reliable, we make no representations as to the accuracy of any information prepared by any unaffiliated third party incorporated herein and take no responsibility therefore.

All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change without prior notice. Investing in the stock market involves gains and losses and may not be suitable for all investors. Past performance is no guarantee of future results.

For additional information about Nottingham, including fees and services, send for our Disclosure Brochure, Part 2A or Wrap Brochure, Part 2A Appendix 1 of our Form ADV using the contact information herein.